500% in 8 Years. It Happened Once. The Setup Just Reappeared.

From 2003 to 2011, Chile returned 500% in USD terms. The valuation, the commodity backdrop, the political inflection...it's all lining up again. Here's the trade.

There’s a country sitting at the bottom of South America that the market has spent the better part of fifteen years actively ignoring. No love. No analyst upgrades. No breathless CNBC segments. Bugger all institutional attention whatsoever.

Which is, of course, precisely why we’re interested in Chile.

The Setup Nobody’s Talking About

Let me give you the picture in numbers first, because the numbers are remarkable.

The iShares MSCI Chile ETF (ECH) recently completed a long-term bottoming process...the kind of base that takes years to build and is painful to watch. Relative to the S&P 500, Chilean equities are trading at half the level they were during the LTCM and Russian default crisis in 1998. Half. That was one of the most chaotic moments in modern financial history, and Chile is cheaper now relative to US equities than it was then.

Fifteen years of underperformance. Forward P/E of 14x. A commodity-rich economy with copper accounting for roughly 50% of its exports.

And a brand-new pro-business government just swept into power in a landslide.

In other words, we have deeply unloved equities, a generational valuation low, a commodity tailwind building for years, and a political catalyst. All arriving at the same time.

Call us hopeless romantics, but we love this setup.

What Chile Actually Is

Here’s what most investors miss. Chile isn’t really an equity market story. It’s a commodity story dressed up as an equity market.

Copper is the spine of this economy. It runs through everything...the mining sector, the government’s fiscal capacity, the current account. And copper, like most commodities, spent the last decade getting absolutely smashed. Capital starvation.

No new mines permitted. Existing operations stretched thin. The infrastructure to bring new supply online takes a decade minimum, and the industry has been in capital hibernation mode since the commodity bear market bottomed around 2015-2016.

Now AI is showing up and demanding copper in quantities that strain credulity. Data centres. EV charging infrastructure. Grid upgrades for power systems that the so-called “green transition” was supposed to build but largely hasn’t. Every one of these things is a copper consumption story. Supply is structurally constrained. Demand is structurally rising. You do the arithmetic.

Chile sits on top of the world’s largest proven copper reserves. It isn’t going anywhere.

The Historical Precedent

Now let me show you what happens when a commodity-rich emerging market inflects after a prolonged bear market.

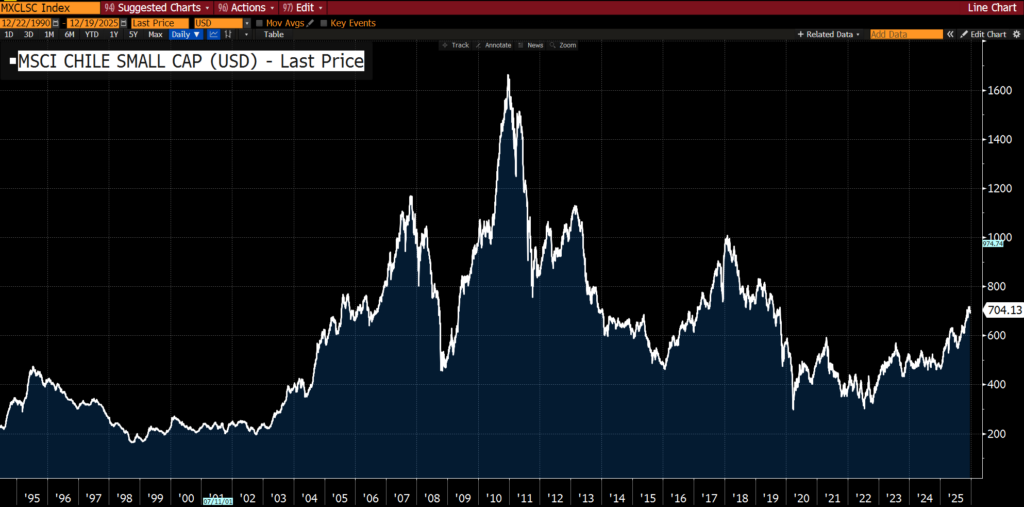

From 2003 to 2011, the large-cap Chilean equity market went up approximately 500% in USD terms. Five hundred percent. That wasn’t some leveraged derivative play or crypto moonshot. That was a country ETF, available on any brokerage account, for anyone paying attention.

Small caps did 700%.

We are not saying history will repeat exactly. It never does. But we are saying the setup rhymes ... and rhymes loudly. The commodity underperformance relative to the S&P 500 is as extreme now as it was at the late-1990s peak of the TMT bubble.

Emerging markets as a whole are trading at relative lows not seen in a generation. The rotation hasn’t happened yet. That’s the whole point.

The opportunity lives in what hasn’t happened yet.

The Political Catalyst

The election of José Antonio Kast changes the operating environment in ways that matter for investors.

Chile spent years under heavily socialist leadership. The previous regime’s approach to mining investment was, shall we say, not conducive to attracting foreign capital.

Legal certainty...the thing miners need more than almost anything else before committing a billion dollars to a project...was, diplomatically speaking, a dog’s breakfast.

The new administration is doing something radical: simplifying the tax system, reducing compliance costs, creating legal certainty in mining, and actively pursuing foreign investment. This is the pro-business playbook, and it works...particularly when commodity prices are already setting up for a multi-year run regardless of what any government does.

The political tailwind doesn’t create the trade. It amplifies it.

Think of it this way. The commodity supercycle would give Chilean equities a tailwind regardless. A socialist government was a headwind. The new government removes the headwind. That’s not additive to the thesis...it’s multiplicative. You’re now running downhill with the wind at your back, and you were already starting from the cheapest valuation in a generation.

The Grand Rotation

Zoom out further and you can see what’s actually happening here.

We have been saying the same thing since Insider launched: emerging markets and commodity-sensitive stocks are going to have their day. That day is not far off. The S&P 500 is priced for perfection at over 23x price-to-cash-flow...richer even than the dot-com bubble peak. The Mag 7...sorry, the Bag 7...have become so correlated via their mutual AI investments that a stumble in one is increasingly a stumble in all. Passive flows have done a remarkable job disguising this until now.

Meanwhile, emerging markets have underperformed the S&P 500 by extraordinary margins for fifteen years. MSCI EM is sitting at relative lows that mirror exactly where it was at the height of the TMT mania in the late 1990s...and we all remember what happened after that.

The 2001-to-2011 period saw a decade of EM outperformance so dramatic that most investors who lived through it still can’t quite believe it. We believe it’s coming again. Chile...with its copper exposure, its political reform story, and its rock-bottom relative valuation...is one of our highest-conviction expressions of that thesis.

The Entry Point

For those who want direct exposure to Chile, the most straightforward entry point is the iShares MSCI Chile ETF (ECH), trading on the NYSE. It’s your one-stop copper-and-Chile vehicle. At 14x forward P/E...with the underlying components also averaging around 14x...this is not a stretched valuation. Far from it.

Do your own research. This is what we own (the ETF) and why we own it. It is not advice for you specifically...your circumstances are different from ours, and all investments carry risk, including the possibility that we are dead wrong and/or just very early (which sometimes looks the same as being wrong, for years).

The Bottom Line

Chile has everything I prefer in an investment. It’s cheap. It’s unloved. It’s been terrible for a decade. The dominant sector is structurally undersupplied relative to demand. The political environment just flipped from headwind to tailwind. And the macro backdrop...a grand rotation out of US equities and into commodities and emerging markets...is the strongest structural setup I’ve seen since the early 2000s.

Fifteen years of underperformance is not a red flag. It’s the prerequisite.

The folks who bought the S&P 500 in 2000 at 30x earnings waited a long time to get back to even. The folks who bought cheap, unloved emerging markets in 2001 and held through 2011 made five to seven times their money.

History has a wry sense of humour. We’re smitten with the idea that it’s about to repeat.

As always, do your own research.

This ETF has no KID in English. How would one then go about to be able to buy?