The $40 Billion Bid for a sub $100 Billion Market

JP Morgan built a bond index in 1992 to measure how much investors hate a country. Argentina recently hit levels that could force $40B into a $100B market. Are you paying attention?

Greetings, friends!

I mentioned this at our Mavericks event in Cayman last year. That when Argentina’s risk index drops sufficiently to be included in the emerging market status, there would be an immediate auto-execute bid for...by my calculations...at least $40 billion of capital.

Keep in mind that the entire market is still sub $100 billion.

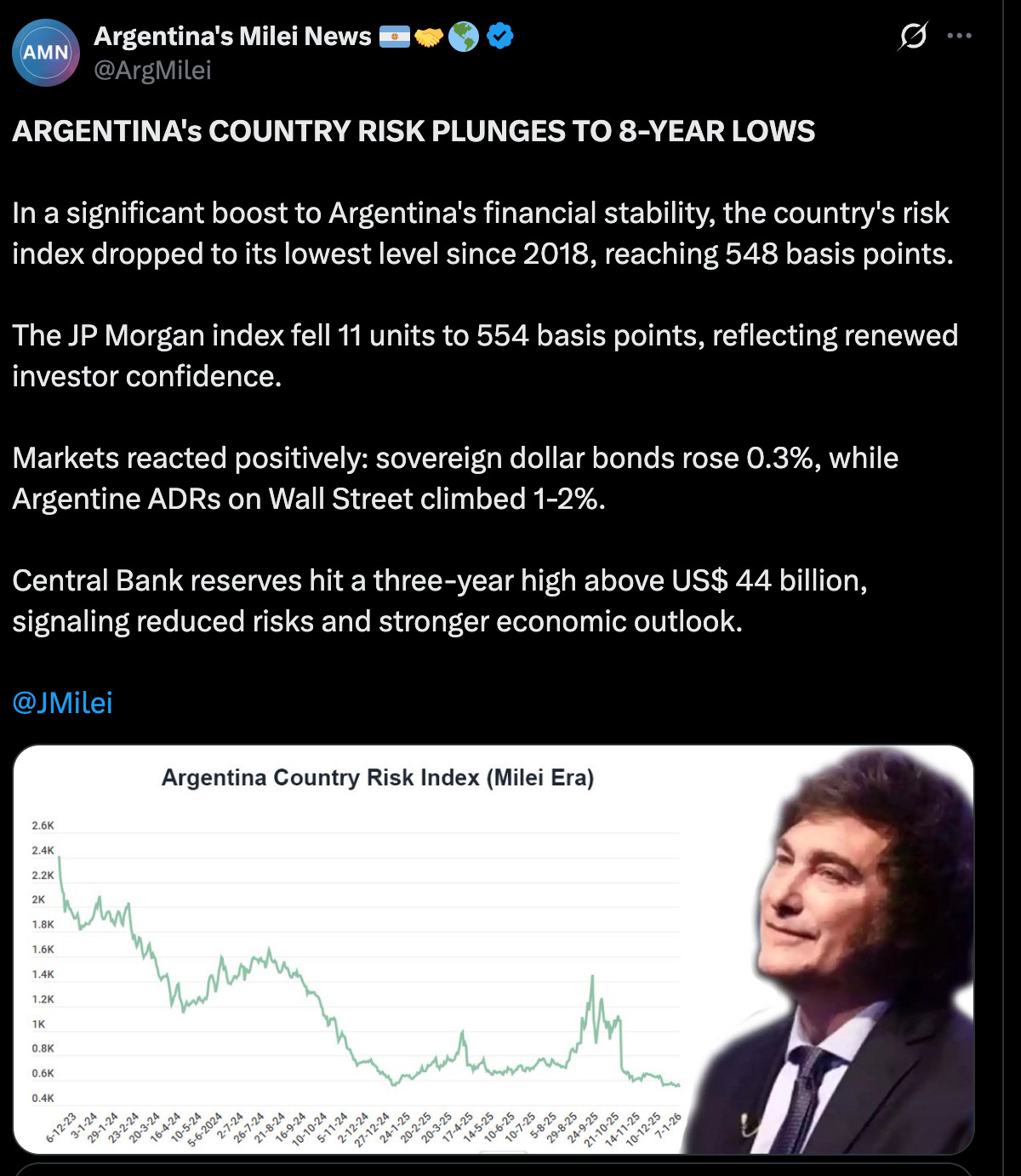

And here we are. The JP Morgan EMBI+ Argentina recently hit 548 basis points. An eight-year low. Down from 1,920 when Milei walked through the Casa Rosada door in December 2023.

Let’s talk about what that number actually means. Because most people hear “country risk index” and glaze over. Which is precisely why most people are going to miss this.

The Scoreboard Nobody Taught You to Read

Back in 1992, JP Morgan created the Emerging Markets Bond Index...the EMBI...originally to track Brady bonds. Those were the restructured sovereign debt instruments issued by developing countries after the 1980s Latin American debt crisis. Named after US Treasury Secretary Nicholas Brady, they were the debt-restructuring mechanism that gave countries like Argentina, Brazil, and Mexico a path back to capital markets.

The original EMBI covered these Brady bonds only. By 1995, JP Morgan expanded it into what we now call the EMBI+, adding dollar-denominated loans and Eurobonds. Today it’s the most widely watched sovereign risk gauge on the planet.

Here’s the elegant simplicity of it. The EMBI measures the spread...the gap in basis points...between what a sovereign government pays on its dollar-denominated bonds versus what the US Treasury pays on bonds of the same maturity. The Treasury rate is considered the risk-free benchmark. Anything above it is the market’s way of saying: “We need compensation for the risk of lending to you.”

One hundred basis points equals one percentage point. So when Argentina’s spread was sitting at 1,920 bps in December 2023, the market was pricing in a premium of roughly 19.2% above US Treasuries to lend Milei’s government money.

Sheesh.

When it falls to 548 bps...as it now has...the market is saying something very different. It’s saying we trust this government enough to lend to it at roughly 5.48% above a US Treasury. That’s not investment grade. But it’s a different galaxy from where it was.

In other words...the market has voted. And it’s voting for Milei.

Why Is Argentina Falling?

Let me count the ways.

When Milei took office, Argentina was running a fiscal deficit of roughly 5% of GDP. Within a year, he’d eliminated it entirely. Primary surplus. The man actually used the chainsaw. That’s not normal for Argentina. That’s barely normal anywhere.

Then came the IMF’s $20 billion Extended Fund Facility in April 2025, with $12 billion disbursed upfront. The Fund backstop gave foreign creditors their security blanket. Monthly inflation, which had been running above 25% when Milei took office, collapsed to roughly 2% by early 2025.

Capital controls were substantially lifted. Residents can buy dollars again. Companies can repatriate dividends earned from January 2025 onwards. The tax amnesty brought over $10 billion back into the formal banking system...dwarfing the previous Macri-era amnesty. Central Bank reserves climbed to a three-year high above $44 billion.

In October 2025, Milei’s party won the midterm elections in a landslide. Gone was the binary bet that Argentina might revert to Peronism. His mandate was ratified. The risk premium compression that followed was immediate and dramatic...from ~1,080 bps in mid-October to the mid-500s by January 2026.

The country risk fell below 500 basis points in late January 2026...the first time since 2018. For context: market analysts have said Argentina can return to international debt markets “optimally” once the spread reaches the 450–550 range. The country already issued its first dollar bond since 2018 in late 2025...a Bonar 2029 at 6.5%, which was 1.4x oversubscribed.

We are not in a speculative scenario. We are watching a structural change in real time.

The Trigger Nobody Is Pricing In

Here’s where it gets interesting. The EMBI is a bond spread. What matters for capital flows...specifically the tidal wave I’m describing...is something slightly different: the MSCI market classification.

Let me connect the dots.

In November 2021, MSCI demoted Argentina from Emerging Markets to Standalone Market status...the bottom of the barrel. The reason was simple: the Fernandez government had imposed capital controls so severe that international institutional investors couldn’t replicate the index. Couldn’t move money in. Couldn’t move money out. So MSCI removed Argentina from the emerging markets universe entirely.

Most mainstream institutional capital has a mandate. They can only invest in markets that sit inside certain classifications. Standalone Market means: you don’t exist for the vast majority of global institutional money.

Roughly $893 billion now sits in emerging markets ETFs globally. That’s passive tracking alone. Add active EM funds, EM bond funds, global macro allocations, and sovereign wealth funds...and the total pool of capital that requires emerging market classification to invest is orders of magnitude larger. The MSCI Emerging Markets index alone has approximately $384 billion passively tracking it.

MSCI typically reviews classifications in June each year. Per analysis from Latam Advisors CEO Sebastián Maril, the earliest Argentina could be added to the watch list is June 2026...with reclassification possible in June 2027. The timeline is not tomorrow. But the trajectory is unmistakable. And the capital market doesn’t wait for MSCI to make it official.

This is important. The opportunity is not in buying Argentina after the MSCI upgrade. It’s in buying Argentina before the announcement.

Invest in the same asymmetric opportunities we are:

When the Gates Open: Historical Precedents

We’ve seen this movie before.

In 2014, Qatar and the UAE graduated from MSCI Frontier to Emerging Market status. In the twelve months between the announcement and the effective date, the UAE stock market surged +99%. Qatar rose +54%. Pakistan, upgraded in 2017, rose +28% in the pre-inclusion period.

In other words...the smart money gets in before the date is announced. And the passive money, constrained to buy at the effective date, arrives late to a party already priced. That’s not a criticism of passive investing. It’s just a description of how the mechanics work.

The reason is structural. International asset allocations benchmark to indexes. As those indexes change, hundreds of billions of dollars must rebalance mechanically. Funds that track the MSCI EM index have no discretion. If Argentina is in the index at 0.2% weight, they must own it at 0.2% weight...on the effective date. Period.

The front-runners know this. The active managers who can invest ahead of the date know this. Hedge funds know this. They buy before the announcement. The passive funds show up on settlement day and buy whatever is left, at whatever price it’s trading.

Now here’s the wrinkle with Argentina that makes this specific opportunity different.

Not Enough Assets to Buy

Argentina’s total listed market is still sub-$100 billion. The MSCI Argentina index at Emerging Markets weighting would include only four companies in the standard index: YPF, Grupo Financiero Galicia, Banco Macro, and Pampa Energía. Eleven names in the small-cap index.

Even accounting for active EM mandates and bond market flows, once the capital flood starts...and I estimate at least $40 billion when you include the full spectrum of passive trackers, active mandates, sovereign funds, front-runners, and bond index inclusions...there simply aren’t enough listed assets to absorb it.

You cannot put $40 billion into a $100 billion market at 0.2% weight through only four liquid large-caps. The math doesn’t work.

So what happens? The capital doesn’t disappear. It goes hunting. And where it goes hunting is private equity.

This is where the real asymmetry lies. The wave of capital that will enter private equity will dwarf what we’ll see in listed equity.

Argentina’s private infrastructure is still massively undercapitalized relative to its resource base. Vaca Muerta is the second-largest shale gas reserve and fourth-largest shale oil reserve in the world...barely scratched. Agricultural land. Energy services. Banking infrastructure recovering from decades of suppressed credit. The RIGI investment promotion regime...which expires at end of 2026...offers legally binding 30-year guarantees on tax, FX, and capital repatriation for investments over $200 million. The clock is ticking.

I’ll remind you: we have been positioned in Argentina since 2021. We have three private equity vehicles in the country...Vaca Muerta accommodation infrastructure, farmland, and YPF non-core oil well development. We put those positions on when the EMBI was near 1,700 and the country risk made most institutional investors physically nauseous.

The same people who were nauseous then are the same people who will be buying in 2027...at higher prices, through passive vehicles, with bugger all edge.

The Templeton Reminder

I’ve said it before and I’ll keep saying it. Sir John Templeton underperformed the S&P 500 for thirteen consecutive years before generating a 3x return in the 1970s. The biggest risk to a value investor isn’t being wrong. It’s losing patience before being proven right.

Argentina has been good to us despite testing our resolve since 2021. It continued to test resolve through the Fernandez capital controls, the 211% inflation peak, and every “Argentina is uninvestable” headline the financial press could churn out.

Those headlines were the signal, not the noise.

The country risk index now sits at an eight-year low. The fiscal picture is the cleanest it’s been in a generation. A man actually wielded the chainsaw and survived a democratic election. The IMF is providing cover. The US Treasury is buying pesos.

And the MSCI clock is ticking toward a reclassification that will force hundreds of billions of dollars to take notice of a market worth less than $100 billion.

In other words...the spring is coiled. And compression breeds violence.

Do your own research. This is not investment advice. These are our positions and our reasoning...your situation is different from ours.

But I’ll say this plainly: the people who are waiting to see how this plays out are going to be buying from the people who bought when it was obvious only to a handful of us staring at the data.

That’s usually how it goes.

A vindication of abandoning big government socialism - with all its corruption and destruction of incentives - in favour of Austrian free market economics?