Aliens? But Why?

What do you do when the financial system is hanging by a thread and about to collapse?

Aliens? But Why?

Greetings, friends!

What do you do when the financial system is hanging by a thread and about to collapse?

Why, of course, you call on an alien invasion.

I’m sure it’s got nothing to do with this…

Hedge funds…including ours…know what’s coming.

The Bank of England and the Ultimate Shock Scenario

If a government ever rolled out an official disclosure in a way that genuinely shook people, the real impact wouldn’t be aliens. It would be permission. Permission to say the old rules no longer apply. Permission to move fast, centralize decisions, and explain later.

It’s what happens in every crisis. And if you need to get these things done, it is logical that a crisis is needed. If needed badly enough…then created.

This leads us to false flags. And false flags, despite what the fact-checkers would have you believe, are not the province of tin-foil-hat merchants on the internet. They are a recurring feature of recorded history…used by governments for centuries to take nations to war, justify emergency powers, and silence opposition.

The examples are not subtle.

The Reichstag Fire of February 27, 1933 is probably the cleanest. Someone set the German parliament building alight. Hitler immediately blamed the communists, and within days President von Hindenburg signed an emergency decree suspending civil liberties across Germany. The Communist Party’s parliamentary delegates were arrested. Seats cleared. Hitler’s National Socialist party went from plurality to majority…and never looked back. Whether the Nazis lit the match themselves remains debated by historians. What is not debated is what followed: the fastest consolidation of executive power in modern democratic history. One building. One decree. Game over.

Then there’s the Gulf of Tonkin incident of August 1964. The US National Security Agency claimed North Vietnamese torpedo boats attacked the USS Maddox…twice. Congress passed the Gulf of Tonkin Resolution, granting President Johnson broad authority to wage war in Vietnam without formally declaring it. Over 58,000 American soldiers died in what followed. Then, in 2005, declassified NSA documents confirmed what insiders had known for decades: the second attack never happened. Radar ghosts. The war that consumed a generation was greenlit on an event that did not occur.

staged by Nazis on 31st August 1939. Along with some two dozen")

And lest you think this was uniquely American creativity: in 1939, Nazi SS troops staged an attack on a German radio station at Gleiwitz, dressed in Polish uniforms and planted bodies as evidence. It provided the pretext for the German invasion of Poland. The Second World War began with a theatrical production.

There’s also Operation Northwoods — a 1962 US military plan, declassified in the 1990s, which proposed staging terror attacks on American soil and blaming Cuba to justify an invasion. Fake funerals. Remote-controlled planes painted as civilian airliners. The whole thing. President Kennedy rejected it. But the fact that it was conceived at the highest levels of the Pentagon…put on paper and formally proposed…tells you everything about how power thinks when it needs a pretext badly enough.

The pattern is not complicated. Crisis creates fear. Fear suspends judgment. Suspended judgment creates consent. Consent enables action that would otherwise be impossible. This is not conspiracy thinking…it is the documented playbook of state power across centuries.

Remember the Convid plandemic. You would certainly die without lockdowns and the poison shots…fear. And to add to it, you’d be killing granny…shame and guilt. It’s ancient. It works every time.

When people are scared and disoriented, they don’t ask for elegant policy. They ask for stability. And they’ll often accept limits they would normally resist, simply because uncertainty feels worse than control.

When the Numbers Stop Making Sense

Markets are simply the collective decisions of many people, and people are emotional creatures who build their lives on stories and expectations. This is why markets price stories, not just numbers. But what happens when the stories break?

Think of any boom. At some point it almost always becomes irrational. The numbers stop making sense. Then they price stories about growth, safety, and institutional competence.

The history of this is long and consistent. And it never stops being instructive…because the psychology that drives it doesn’t change.

The Dutch Tulip Mania of 1636–37 is the canonical case. Tulip bulbs…flowers…became a speculative vehicle. At the peak, certain rare varieties were trading for the equivalent of a skilled tradesman’s annual salary. Forward contracts required no margin. Anyone with a pulse could speculate. Eventually someone showed up at an auction and refused to pay the expected price. The whole thing collapsed in days. The phrase “greater fool” exists because of what happened in that Dutch winter.

Across the Channel a century later, the South Sea Bubble of 1720 achieved something similar. The South Sea Company…granted exclusive trading rights in South America by the British government…saw its shares soar on rumors and insider dealing. The mania swept through British society. Sir Isaac Newton, the man who gave us gravity and calculus, reportedly lost a substantial sum. He is said to have remarked: “I can calculate the motions of the heavenly bodies, but not the madness of people.” Newton. The smartest man alive at the time. Destroyed by narrative.

The 1840s brought Railway Mania in Britain — frenzied investment in railway companies, fuelled by genuine excitement about a transformative technology. Sound familiar? Companies rushed to build thousands of kilometres of track far outpacing any sustainable demand. When it collapsed, companies failed across the board, enormous debts were left behind, and investors were ruined. The technology was real. The valuations were codswallop.

Then came the dot-com era. The Nasdaq in early 2000 was pricing stories about disruption and a new economy where traditional valuation metrics simply didn’t apply. From March 2000 to 2003, the Nasdaq fell 80%. The S&P 500 and Russell Growth fell 45% and 50% respectively. Value stocks, by contrast, were up 7%. The boring, unloved, numbers-actually-make-sense stuff. Imagine that.

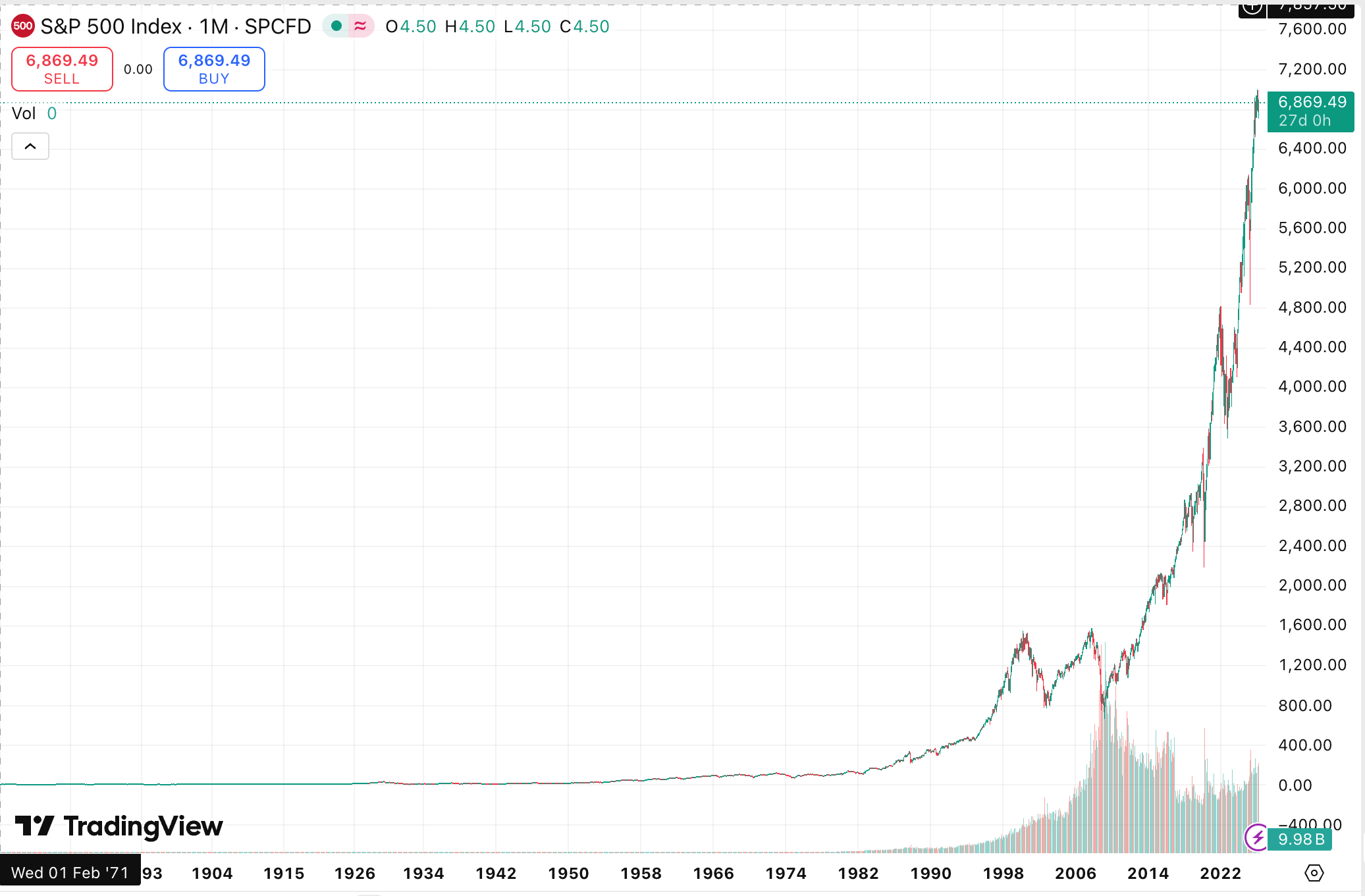

Today, the S&P 500 sits at a price/cashflow of 23x. The peak of the dot-com bubble…which we just described as an 80% Nasdaq wipeout…was 15x. In other words, the current US market is roughly 50% more expensive than the most irrational moment of the internet bubble. And the story holding it all up? Artificial intelligence…genuinely transformative technology, just like the railway, just like the internet. The technology may be real. The valuations are something else entirely.

Gravity isn’t a risk…it’s a schedule.

🔴 Invest in the Same Asymmetric Opportunities We Are…

When the Story Breaks: What Happens Next

A reality-shattering event doesn’t just move prices; it breaks the story itself. When that happens, you get volatility, a rush toward anything that feels safe, stress in banks and payment systems, and eventually spillover into the real world. That’s what the former Bank of England analyst is really describing. Not science fiction…fragility.

The historical case studies here are unambiguous.

When the story broke in 1929, investors fled to cash and gold. The Dow Jones lost almost two-thirds of its value. Meanwhile, Homestake Mining…then the largest gold producer in the United States…delivered over 500% capital appreciation between October 1929 and December 1935, even as the broader market was being destroyed. Five hundred percent. Gold stocks initially fell with everything else, as they always do in the first wave of liquidation panic. But then they became the trade of the decade.

When 2008 arrived, the same pattern repeated. Global stocks fell 49%. US Treasuries gained 17%. Gold rose 47%. The US dollar, Japanese yen, and Swiss franc soared against most major currencies as the world’s investors scrambled for any anchor of perceived stability. Currencies that felt safe. Countries that felt solvent. Assets that felt real.

But here is where the current moment diverges from the history books.

In 2008, investors could flee to US Treasuries and call it safety. The US government was still considered creditworthy. The dollar was the unquestioned reserve currency. The flight-to-safety playbook had a clear destination.

Today? The Bank of England is warning about hedge funds holding £100 billion in gilt bets. Sovereign debt…the traditional safe haven…is itself the problem. Global bond yields are simultaneously at multi-decade highs. Four drivers, none of which are going away: soaring deficits, sticky inflation, central bank credibility collapse, and geopolitical pressure reducing foreign demand. Bond vigilantes are already active. When the traditional safe haven is the problem, the flight-to-safety playbook gets rewritten.

And capital, as it always does, starts sniffing this out ahead of the headlines.

Just look at gold and silver…

Capital has been voting with its feet. Not because of inflation expectations…gold’s relationship to CPI is notoriously unreliable as a timing tool. But because of something more fundamental: loss of faith. Gold moves on loss of faith in institutions, in fiat, in the competence of the people running things. We are watching that unfold in real time.

And geographically…

The East is building financial architecture that routes around Western systems. Hong Kong and Shanghai positioning themselves as the global gold trading center. This is the geographic expression of the same capital migration…away from Western sovereign debt, toward hard assets and Asian economies with actual manufacturing, actual energy production, and actual balance sheets.

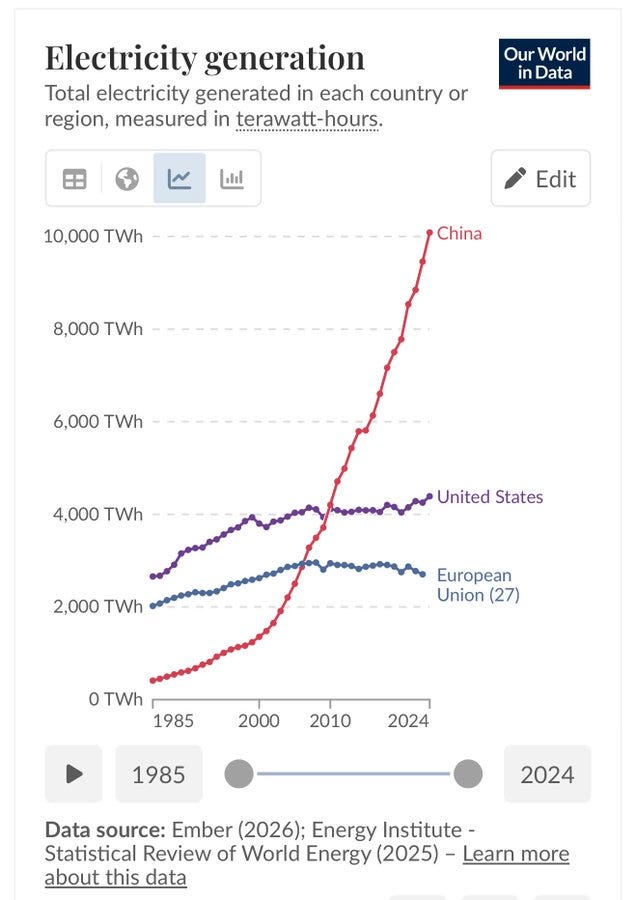

And I’ve not even touched on energy, which is life. China now generates 40% more electricity than the US and EU combined.

The correlation between energy and living standards is well documented. At this point, based purely on that, you’d be betting on Asia…China in particular…over the EU or US. That’s before looking at valuations or any other metric. When you do, the answer becomes even more obvious.

Reframing This Through the Bank of England Lens

Now, let’s flip the lens. If authorities needed that destabilization as cover, a disclosure-style shock becomes a master key. You can introduce emergency measures without calling them permanent. You can blame instability on “the event” instead of past policy mistakes. You can centralize decision-making because coordination suddenly sounds like survival. And the stranger the event, the fewer people argue the details. Nobody debates balance sheets when they’re trying to re-anchor reality.

History indicates that societies rally around threats. Fear unifies behavior faster than persuasion. This is why you’ll see politicians driving fear. It is ancient, and it works every time.

Project Blue Beam was a theory popularized in the early 1990s by Serge Monast, which claimed that advanced technology could be used to simulate a massive religious or extraterrestrial event in order to unify populations under centralized authority. There’s no credible evidence such a project exists…but that’s almost beside the point. What it captures is a logic of power: spectacle creates fear, fear suspends resistance, and consent follows faster than debate ever could.

This all sounds like a World Economic Forum wet dream. War and crisis have always been the fastest paths to expanding authority. Seen through that lens, disclosure wouldn’t be about knowledge. It would function as a global threat narrative…one that makes consolidation and control feel not just acceptable, but necessary.

Remember: fear that overwhelms normal reasoning can be used to justify sweeping changes in governance.

Viewed this way, the Bank of England is acknowledging how fragile the system already is. Trust is thin. Narratives move faster than institutions. And once belief breaks, authorities suddenly have cover for actions that would normally be politically impossible.

A disclosure-style shock would provide that cover instantly. Strip away the conspiracies and the core point is simple: markets don’t fail because numbers change…they fail because belief collapses.

And if anyone ever needed a fast excuse to centralize power or expand emergency authority, a shock to belief would do it. That doesn’t prove a plan exists…it explains why the idea lingers, and why systems built on trust quietly fear the moment trust itself becomes the variable.

The Reichstag burned in 1933. The Gulf of Tonkin happened…or didn’t…in 1964. These are not stories from the fever swamps of the internet. They are declassified history. The pattern is old. The stakes today are simply higher.

Position accordingly. Do your own research. Or join us inside Insider where we do most of the research for you. 👇🏻👇🏻👇🏻👇🏻👇🏻